Weekly Market Commentary – 7/29/2022

-Darren Leavitt, CFA

Investors faced the busiest week of the year as 175 companies representing 50% of the S&P 500’s market capitalization reported 2nd quarter earnings. The results were mixed and produced drastic swings in share prices. Microsoft and Alphabet reported “better than feared” results, while Amazon and Apple provided better than expected results. Chevron and Exxon both crushed their earnings estimates. On the other hand, Meta, Walmart, Shopify, Roku, and Intel were disappointments. Growth issues outperformed over value, and the Mega-caps outperformed their counterparts.

Investors were also faced with the July Federal Open Market Committee’s decision on monetary policy and the subsequent statement from Fed Chairman Jerome Powell. The Committee unanimously decided to increase the policy rate by 75 basis points to a range of 2.25% to 2.50%. The market rallied on the Fed Chairs’ comments that it may be appropriate to wait and see how inflation has been impacted by the front loading of the Fed Funds rate. The Chairman also suggested that the Fed would be data-dependent and willing to go another 75 basis points in the September meeting. However, it will not telegraph its policy to the markets as it has over the last several years. The results will increase the importance of data analysis by the street and likely cause more volatility around key economic reports. Unfortunately, the Fed continues to be in a rock and hard spot as they try to thwart inflation by tightening financial conditions while, at the same time, the markets are loosening financial conditions.

Economic data for the week was highlighted by the advanced reading of 2nd quarter GDP, which showed a contraction of 0.9%. The street had been looking for growth of 0.5%. The final reading of Q1 GDP showed a contraction of 1.6%. If the Q2 readings continue to show contraction, there is an argument that we are technically in recession. The debate of whether or not we are in a recession will take on many forms, but the most prominent rebuttal to the notion that we are currently in a recession is based on a continued strong employment market. Initial claims for the week came in at 256k versus the street’s estimate of 253K. Continuing claims fell by 25k to 1.359M. Inflation data included the Federal Reserve preferred measure of PCE, which came in at 0.6%, in line with estimates but up 6.8%, the highest level since 1982. Core PCE was also in line with expectations at 0.5%. The Employment Cost Index ticked higher to 1.3% versus the consensus estimate of 1.1%. Personal Income increased by 0.6%, slightly higher than the 0.5% consensus. Personal spending increased by 1.1%, which was also higher than estimated. The final reading of the University of Michigan’s Consumer Sentiment plummeted to 51.5%, the 2nd lowest reading ever.

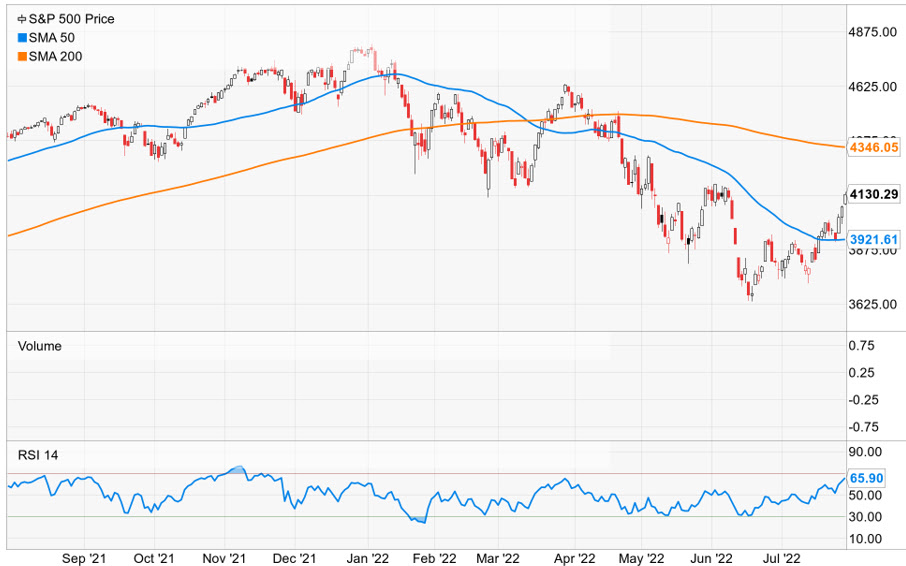

The S&P 500 gained 4.3%, the Dow rose 3%, the NASDAQ increased by 4.7%, and the Russell 2000 added 4.3%. The US Treasury curve inverted further, with the 2-year note yield falling nine basis points to 2.90%. The 10-year yield fell fourteen basis points to 2.64%. As mentioned before, the lower rates across the curve loosen financial conditions. Oil prices traded fractionally higher. WTI increased by $0.61, closing at $98.55 a barrel. Gold prices increased by 4.7% or $80.2 to $1783 an Oz. Copper prices soared by 10.5% to close at $3.57 an Lb. The US dollar weakened against the majors and lost significantly against the Japanese Yen.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.