Weekly Market Commentary – 1/7/2022

-Darren Leavitt, CFA

US financial markets fell in the first week of 2022 after the S&P 500 hit an all-time high on Monday. The release of the December Federal Open Market Committee minutes revealed a much more hawkish Fed. It caused concerns regarding the path of interest rates, which hammered growth stocks and induced a familiar rotation into cyclical issues. Suggestions that the Fed would start reducing its balance sheet sooner and faster than the previous period of normalization caught investors by surprise and sent US Treasury yields materially higher. Economic data released for the week only helped bolster the argument for higher rates. Fed Funds futures now suggest a 75% probability that the Fed will increase rates by 25 basis points in their March meeting just as their asset purchase program is scheduled to end. A report out of Bank America conveyed the Fed would likely raise rates by 25 basis points in March and subsequently raise rates by the same amount over the next eight quarters.

Interestingly, the trade out of growth-oriented issues and into cyclicals comes as new Coronavirus infections in the US topped 1 million in a single day. Some estimates suggest that 80% of the US population will have contracted the Omicron variant by the end of February. The rapid rate of infections has inhibited workers from coming back to work, and in Germany and Japan, more lockdown measures have been instituted.

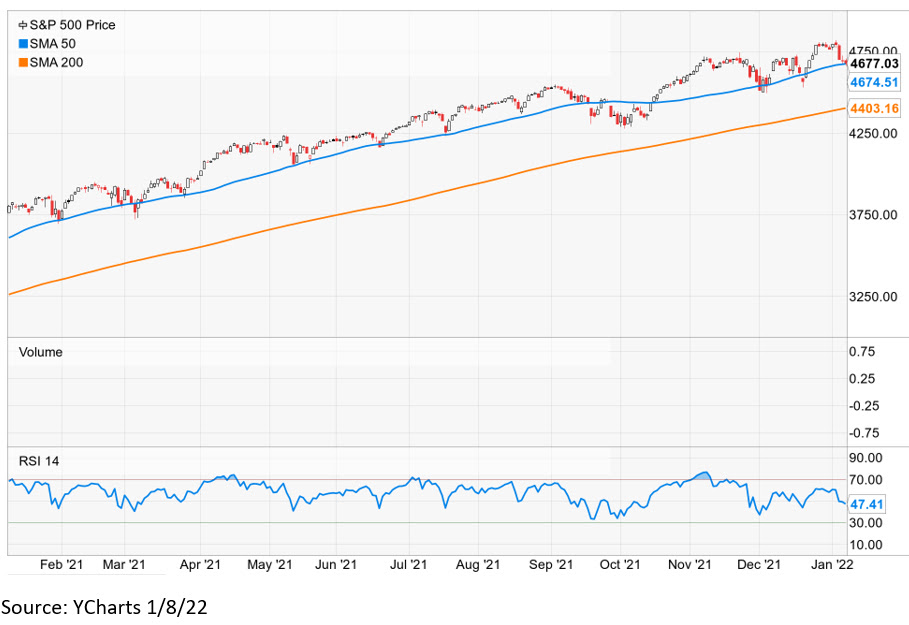

The S&P 500 lost 1.9% for the week. The Dow fell0.3%, the NASDAQ lead declines with a 4.5% loss, the Russell 2000 gave back 2.9%. The US yield curve moved significantly over the week. Of note, the S&P 500 closed just above its 50-day moving average, which has been a solid area of support. A significant breach below this level may bring a more powerful downward market move. The 2-year yield increased fourteen basis points to 0.87%, while the 10-year yield increased a whopping twenty-six basis points to close at 1.77%. The 10-year had touched 1.80%, close to the high yield set last year, and opened the door for 2%. Oil prices moved higher over the week, closing up over 5% to $78.94 a barrel. Gold prices moved in the opposite direction, falling 2% or $38.7 to $1789.4 an Oz. Bitcoin fell over 10% closing down $5,123 to $41,918.

Economic data was headlined by December ISM Manufacturing and the December Employment Situation Report. ISM Manufacturing came in slightly weaker than expected at 58.7%; the street was looking for 60.3%- however, the print still points to expansion. Underneath the number, there were signs that price pressure was improving on an improved supply chain. The Price index came in at 68.2%, down from the prior reading of 82.4%. The Employment situation report showed 199k nonfarm payrolls were created in December; economists expected 475k. Private payrolls increased by 211k versus the consensus estimate of 420k. The Unemployment rate fell to 3.9% from the prior level of 4.2%. Average Hourly earnings were higher by 0.4% above the forecast of 0.3%, and the previous reading was increased to 0.4% from 0.3%. The Average Workweek came in at 34.7, in line with the prior report.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.