Weekly Market Commentary – 11/5/2021

-Darren Leavitt, CFA

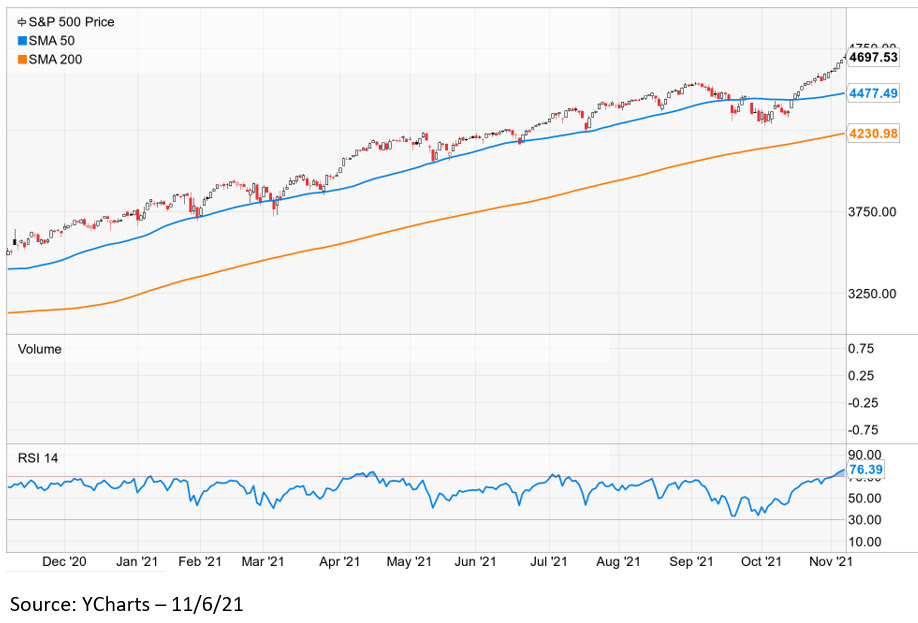

Wow-what a week on Wall Street! US equity indices hit another set of all-time closing highs. Market sentiment was bolstered on several different fronts. 3rd quarter corporate earnings continued to impress, especially in the travel and leisure sector (Uber, Airbnb, Expedia, Bookiing.com), which fostered the “reopening” trade. News that Pfizer’s antiviral pill reduced Covid hospitalizations and mortality by 95% was extremely encouraging. In Washington, there was talk that the much-anticipated infrastructure bill had a real chance to pass in the house, and it did late Friday night and is now off to President Biden’s desk. Global Central banks sent an accommodative tone to the street and tempered inflation expectations, which helped to send yields lower for the week. Economic data for the week was highlighted by a robust Employment Situation report and expansionary manufacturing and services reports.

The S&P 500 gained 2% for the week while the Dow tacked on 1.4%, the NASDAQ increased by 3.1%, and the Russell 2000 crushed it with a 6.1% advance. US Treasury yields fell on reassurances from Fed Chairman Powell that the Fed is in no hurry to raise rates and his expectation that inflationary forces will subside by the 2nd and 3rd quarter of 2022. The 2-year note yield fell ten basis points to 0.39%, while the 10-year bond yield sank eleven basis points to close at 1.45%. Oil prices fell $2.27 or 2.7% to $81.25 a barrel. A build in crude inventories sent crude below $80 early in the week, but OPEC’s announcement that they would maintain its current production levels through December prompted a rebound in prices. Gold prices increased by $33 or 1.8%, closing at $1816.9 an Oz. Copper prices were little changed on the week at $4.342 an Lb.

The economic data calendar was stacked and headlined by the October Employment Situation Report. Non-Farm Payrolls came in better than expected at 531k, and the prior month’s reading was revised higher. Private Payrolls were also better than expected, coming in at 604k. The Unemployment rate fell to 4.6%, which was in line with the consensus estimate but lower than the prior reading of 4.8%. Average hourly earnings increased 0.4% and were in line with expectations and down from September’s increase of 0.6%. On a year-over-year basis, wages are up 4.9%. Initial Jobless Claims fell to another post-pandemic low at 269k, while Continuing Claims fell to 2.105M. ISM Manufacturing for October came in at 60.08, which was down from the prior reading of 61.1, while ISM Services came in at 66.7, which was better than the September reading of 61.9.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.