Weekly Market Commentary – 10/29/2021

-Darren Leavitt, CFA

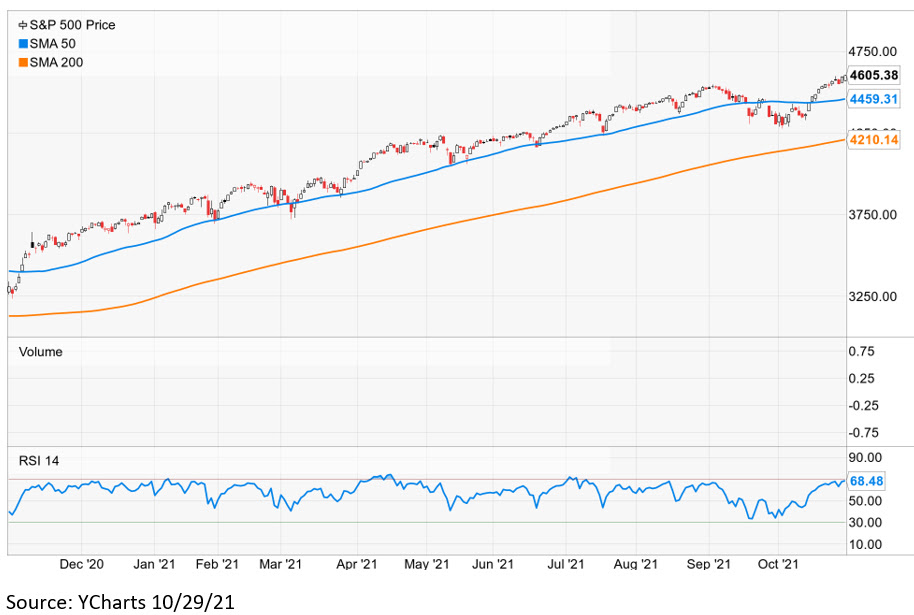

Wall Street faced a deluge of corporate earnings in the final week of October. Generally, reports were better than expected but tempered by management concerns related to the current state of the global supply chain. Tech earnings were mixed with positive market action from Microsoft and Google; Apple and Amazon shares fell in the wake of their announcements. That said, the Mega cap growth issues led the market higher with new all-time highs forged by the NASDAQ and S&P 500. In other corporate news, Tesla topped one trillion in market cap on news that rental car company Hertz has ordered 100,000 cars from the company. Pfizer and BioNTech were granted emergency use authorization of their Covid-19 vaccine for children ages 5 through 11. Facebook announced the company would change its name to Meta effective December 1st. In Washington, President Biden announced the framework for a 1.75 trillion dollar reconciliation bill, but it appears progressives are still not entirely on board. Economic data for the week continued to be mixed.

For the week, the S&P 500 gained 1.3%, the Dow rose 0.4%, the NASDAQ led with an advance of 2.7%, and the Russell 2000 inched higher by 0.3%. The US Treasury yield curve continued to flatten as investors expect the Federal Reserve to increase rates sooner than expected. The 2-year note yield rose two basis points to 0.49%, while the 10-year yield fell ten basis points to 1.56%. Oil prices were little changed on the week, with WTI closing down $0.25 to 83.52 a barrel. Gold prices fell by $12.9, closing at $1783.90 an Oz.

There was plenty of economic data to digest over the week. Q3 GDP estimates fell short of the mark, coming in at 2% versus expectations of 2.4%. Consumer Confidence came in better than expected at 113.8 versus the consensus estimate of 108. In contrast, the final October reading of the University of Michigan’s Consumer Sentiment Index came in below the prior reading. The two data sets showed people encouraged by the pullback in Covid 19 infections, higher wages, and increases in employment opportunities while being worried about inflation. Initial Claims hit another post-pandemic low at 281k as continuing claims trended lower to 2.243 million. Investors will hear from the Federal Reserve in the coming week and await a significant Employment Situation Report scheduled for release on Friday.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.