Weekly Market Commentary – 7/30/2021

-Darren Leavitt, CFA

It was a hectic week on Wall Street as second-quarter earnings continued to roll in with mixed results. Apple, Microsoft, Amazon, Facebook, and Google, which are very influential on the indices, generally sold off in the wake of their announcements. Amazon not only missed Q2 estimates it also lowered guidance for the coming quarter and year. The sell-offs were a drag on the consumer discretionary, information technology, and communication services sectors.

The July Federal Open Market Committee meeting concluded on Wednesday afternoon with assurances from the Chairman that the Fed would remain accommodative for quite some time. There was no change to the policy rate, and the Fed backed away from any timeline related to curtailing its asset purchase program. J Powell said we have a substantial amount of time before the Fed reaches its mandate of full employment. The Fed Chairman’s Q&A session seemed to calm the markets.

Delta variant infection rates continued to spike during the week, especially in areas where vaccination rates have lagged. The spike in infections has caused speculation about the reintroduction of national lockdown mandates that some fear will dampen economic growth.

Economic data for the week was mixed. The Q2 Advanced Estimate of GDP came in lower than expected at 6.5%- the street was looking for 8.2%. New Home Sales missed the mark coming in at 676K versus expectations for 790K. June Durable Goods orders came in 0.8%, while the consensus estimate was 1.8%. Personal Income and Spending were better than expected while PCE prices rose a little less than expected. The Employment cost index rose 0.7% but came in less than the expected 1%. Initial claims regressed again, coming in at 400k. Continuing claims were also higher from a week ago, coming in at 3.269 million. The final University of Michigan’s consumer sentiment for July came in at 81.2 higher than the prior estimate and just better than June’s result.

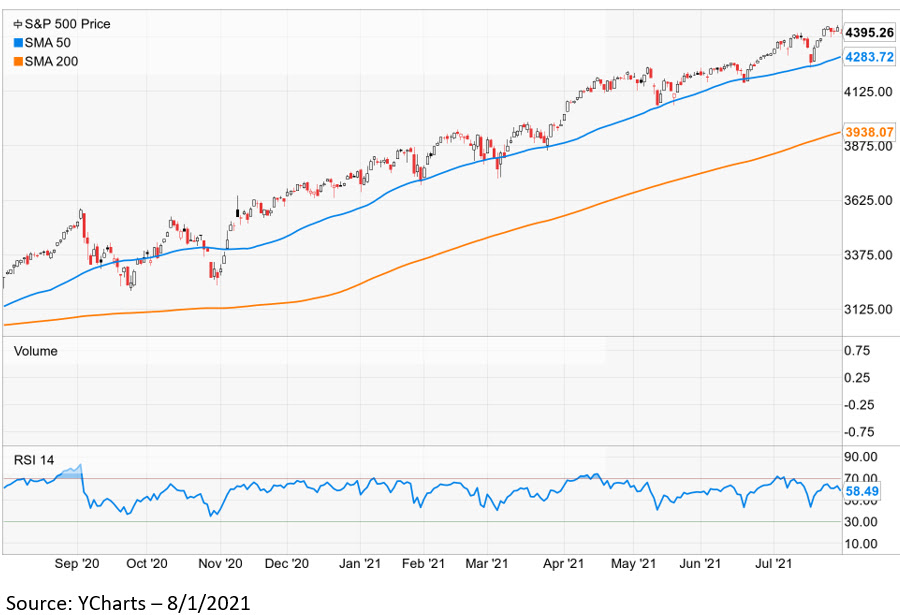

The S&P 500 lost 0.37% for the week while the Dow shed 0.36%, the NASDAQ lagged with a decline of 1.11%, and the Russell 2000 eked out a 0.75% gain. The US yield curve continued to flatten as the 2-year note yield fell one basis point to 0.18%, and the 10-year bond yield fell five basis points to close at 1.24%. Gold prices were essentially unchanged from the prior week closing at 1817.20 an Oz. Oil prices increased as EIA Crude Oil inventories showed a 4.09 million drawdown. WTI closed higher by nearly 3% or $2.11 to $73.87. Copper closed 4% higher to $4.484 per Lb.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.